前言:購房、買車、教育費用...人生中許多重要時刻都需要貸款。但你真的了解貸款背後的計算原理嗎?等額本息與等額本金差在哪?APR 又是什麼?本文將深入淺出地解析貸款計算的核心概念,並提供實用的理財規劃建議,幫助您做出最有利的財務決策。Introduction: Home purchase, car buying, education costs... Many important moments in life require loans. But do you really understand the calculation principles behind loans? What's the difference between fixed payment and declining balance? What is APR? This article will explain the core concepts of loan calculation in simple terms and provide practical financial planning advice to help you make the most beneficial financial decisions.

在開始討論複雜的計算之前,先理解三個核心概念:Before discussing complex calculations, let's understand three core concepts:

1. 本金(Principal)1. Principal

本金是指您向銀行借入的金額。例如購買 1,000 萬元的房屋,自備款 200 萬元,則貸款本金為 800 萬元。本金是計算利息的基礎,每期還款會逐漸減少未償還本金(餘額)。Principal refers to the amount you borrow from the bank. For example, if you purchase a 10 million NTD house with a 2 million NTD down payment, the loan principal is 8 million NTD. Principal is the basis for calculating interest, and each payment gradually reduces the outstanding principal (balance).

2. 利息(Interest)2. Interest

利息是銀行借錢給您的「租金」。計算方式為:Interest is the "rent" the bank charges for lending you money. The calculation is:

每期利息 = 剩餘本金 × 月利率

範例:剩餘本金 800 萬,年利率 2.4%(月利率 0.2%)

第一個月利息 = 8,000,000 × 0.002 = 16,000 元Interest per Period = Remaining Principal × Monthly Rate

Example: Remaining principal 8M NTD, annual rate 2.4% (monthly rate 0.2%)

First month interest = 8,000,000 × 0.002 = 16,000 NTD

隨著本金逐漸償還,每期利息會減少。這就是為什麼貸款前期利息佔比高,後期本金佔比高。As principal is gradually repaid, interest decreases each period. This is why interest makes up a larger portion of early payments, while principal dominates later payments.

3. 利率(Interest Rate)3. Interest Rate

利率有兩種表示方式:Interest rate can be expressed in two ways:

年利率(APR):例如 2.4%,是最常見的表示方式Annual Rate (APR): e.g., 2.4%, the most common expression

利率分為固定利率(貸款期間不變)與浮動利率(隨央行政策調整)。浮動利率通常初期較低,但有升息風險;固定利率穩定,但可能錯過降息機會。Rates are divided into fixed rate (unchanged during loan period) and variable rate (adjusted with central bank policy). Variable rates are usually lower initially but carry rate hike risk; fixed rates are stable but may miss rate cut opportunities.

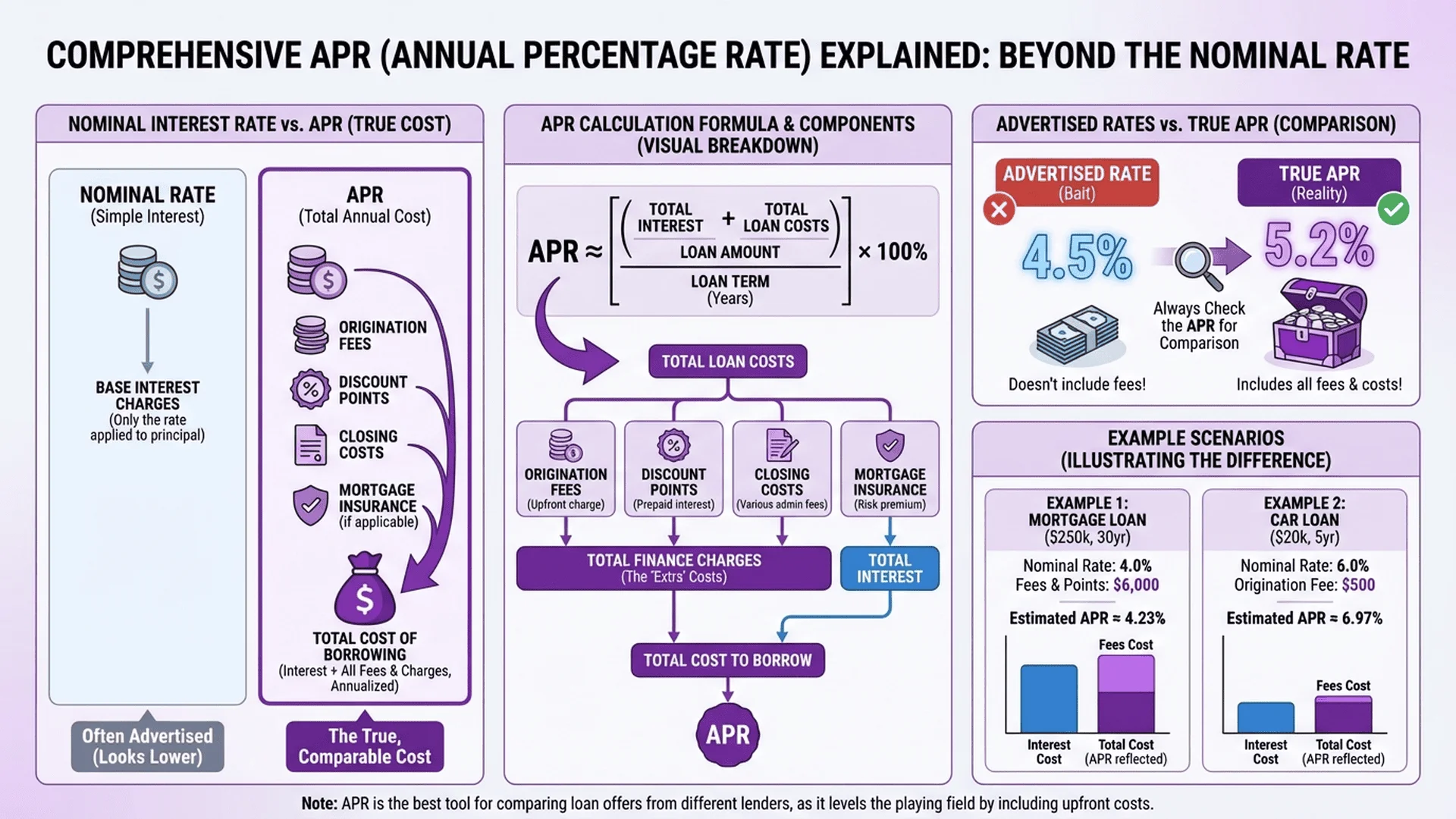

APR 年利率說明圖解,包含計算方式與實際成本分析

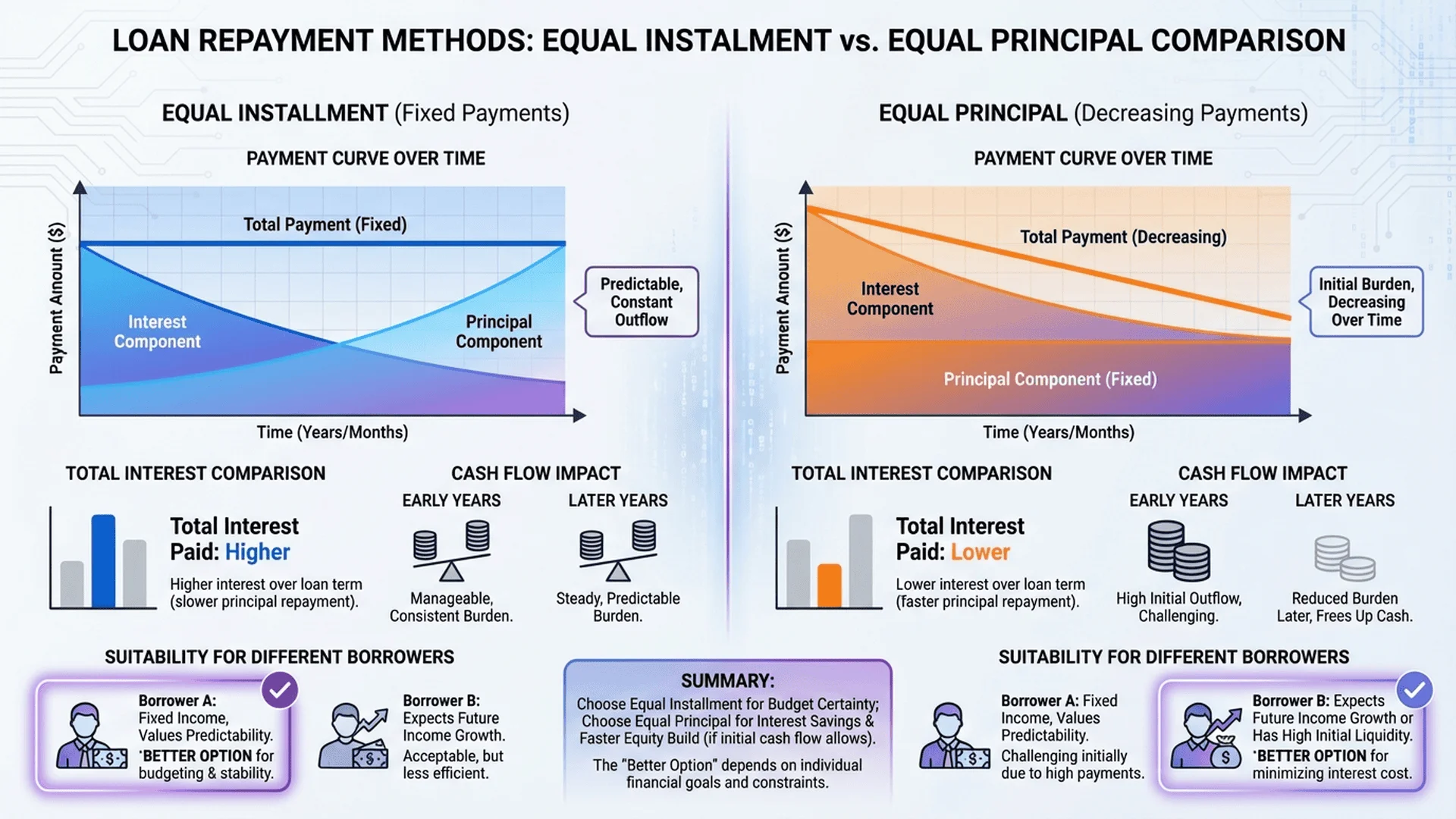

二、等額本息 vs 等額本金:詳細對比2. Fixed Payment vs Declining Balance: Detailed Comparison

這是貸款計算中最重要的選擇,兩種方式還款壓力、總成本差異顯著:This is the most important choice in loan calculation. The two methods differ significantly in repayment pressure and total cost:

項目Item

等額本息(本息平均攤還)Fixed Payment (Equal Installment)

等額本金(本金平均攤還)Declining Balance (Equal Principal)

每月月付金Monthly Payment

固定不變,直到還清Fixed until fully repaid

逐月遞減(首月最高)Decreases monthly (highest in first month)

等額本金:首月 49,333 元(逐月減少),末月 33,400 元,總利息約 192 萬元Declining Balance: First month 49,333 NTD (decreasing), last month 33,400 NTD, total interest ~1.92M NTD

差異:等額本金可省下約 13.8 萬元(6.7%),但初期月付高 7,408 元Difference: Declining balance saves ~138K NTD (6.7%), but initial payment is 7,408 NTD higher

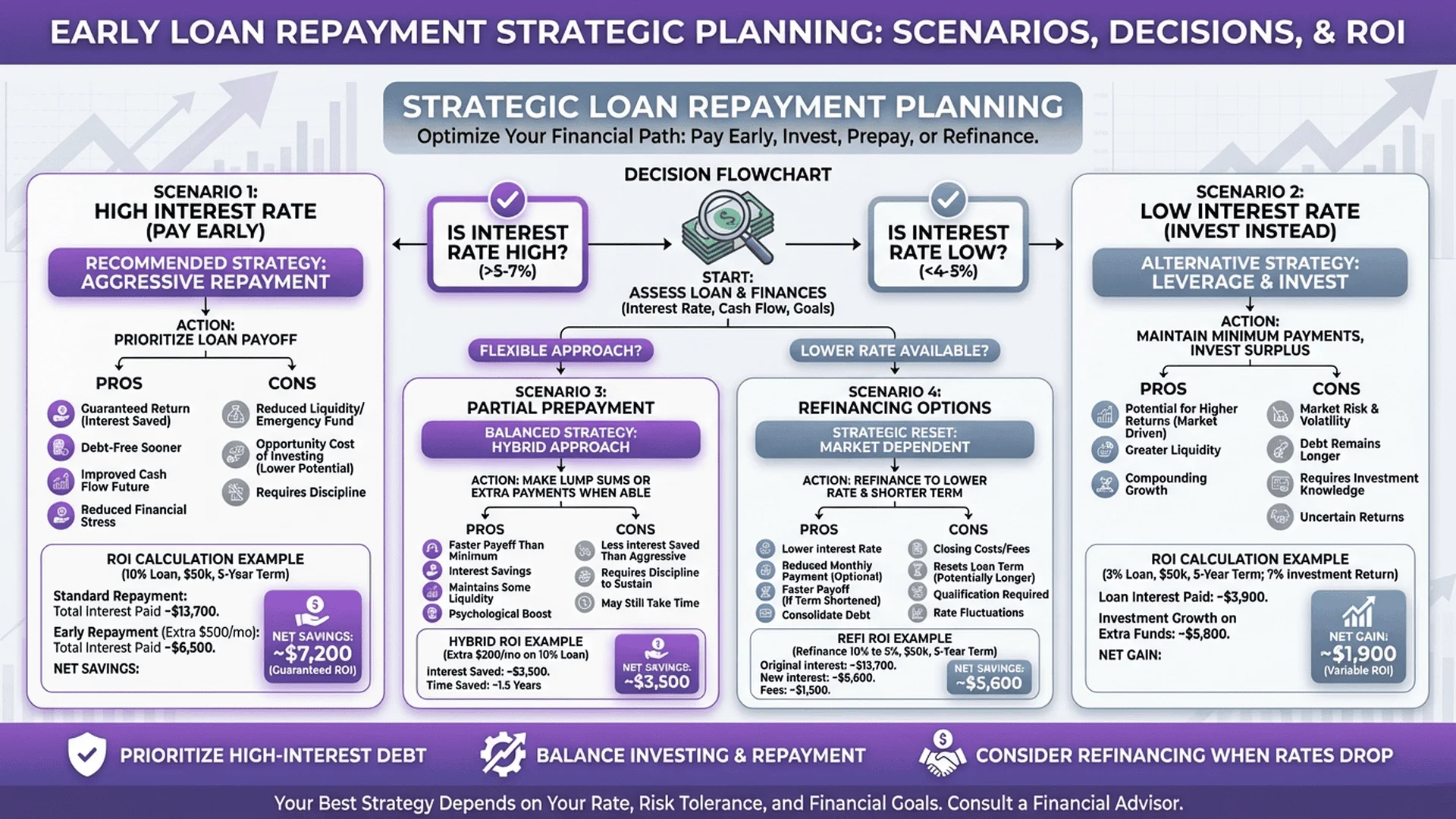

提前還款策略資訊圖表,分析不同情境的最佳還款方案

三、APR(年百分率):真實成本的關鍵指標3. APR (Annual Percentage Rate): The True Cost Indicator

銀行廣告常見「年利率 2.0%」這樣的吸睛數字,但實際成本往往更高。APR(Annual Percentage Rate,年百分率)才是真正的總成本指標。Bank advertisements often feature eye-catching numbers like "2.0% annual rate," but actual costs are often higher. APR (Annual Percentage Rate) is the true total cost indicator.

APR 包含哪些費用?What Does APR Include?

名目利率:銀行廣告的基本利率Nominal Rate: Basic rate advertised by banks

開辦費/手續費:通常 5,000-10,000 元Origination/Processing Fees: Usually 5,000-10,000 NTD

月付金不變,減少還款期數Keep payment, reduce number of periods

年限不變,減少每月負擔Keep term, reduce monthly burden

節省利息Interest Saved

較多(建議首選)More (recommended)

較少Less

現金流壓力Cash Flow

維持原壓力Maintains original pressure

減輕壓力Reduces pressure

適合情境Best For

收入穩定,想早日無債Stable income, want to be debt-free sooner

收入降低,需減輕負擔Reduced income, need lighter burden

3. 提前還款的隱藏成本3. Hidden Costs of Early Repayment

⚠️ 注意違約金!⚠️ Watch Out for Prepayment Penalties!

大多數銀行在貸款前 3-5 年會收取提前還款違約金(通常 1-3%)。例如提前還 100 萬,違約金可能 1-3 萬元。Most banks charge prepayment penalties (typically 1-3%) during the first 3-5 years. For example, prepaying 1M NTD may incur 10-30K NTD penalty.

計算是否划算:Calculate if it's worthwhile:

節省利息:12 萬元Interest saved: 120K NTD

違約金:2 萬元Penalty: 20K NTD

淨節省:10 萬元 ✅ 划算Net savings: 100K NTD ✅ Worth it

五、房貸、車貸、信貸比較5. Comparison: Mortgage, Car Loan, Personal Loan

不同貸款類型的特性與注意事項:Characteristics and considerations for different loan types:

項目Item

房貸(不動產貸款)Mortgage (Real Estate)

車貸(動產貸款)Auto Loan (Vehicle)

信貸(無擔保貸款)Personal Loan (Unsecured)

典型利率Typical Rate

1.8-3.5%

2.5-7%

3-16%

最長年限Max Term

20-40 年20-40 years

3-7 年3-7 years

1-7 年1-7 years

貸款成數LTV Ratio

60-85%(首購可達 8 成)60-85% (up to 80% for first-time buyers)

70-90%

月薪 10-15 倍10-15x monthly salary

擔保品Collateral

房屋(設定抵押權)Property (mortgage lien)

汽車(動產擔保)Vehicle (chattel mortgage)

無(憑信用評分)None (credit score based)

提前還款Early Repayment

通常有違約金(3-5年內)Usually has penalty (within 3-5 years)

部分銀行免違約金Some banks waive penalty

多數免違約金Most waive penalty

稅務優惠Tax Benefits

可抵稅(每年最高 30 萬利息)Deductible (up to 300K NTD interest/year)

台灣自用住宅房貸利息可列入綜合所得稅列舉扣除額,每年最高 30 萬元。假設您的邊際稅率 20%,可節省稅金 6 萬元(30 萬 × 20%)。In Taiwan, owner-occupied mortgage interest can be listed as itemized deductions in income tax, up to 300K NTD annually. If your marginal tax rate is 20%, you can save 60K NTD in taxes (300K × 20%).

條件:(1) 自用住宅;(2) 本人、配偶或受扶養親屬登記;(3) 無出租、營業使用。Requirements: (1) Owner-occupied; (2) Registered under self, spouse, or dependents; (3) No rental or business use.

六、理財規劃建議6. Financial Planning Recommendations

1. 緊急預備金優先1. Emergency Fund First

在考慮貸款前,務必先建立6 個月生活費的緊急預備金。例如月支出 4 萬元,至少準備 24 萬元現金,避免突發狀況(失業、疾病)導致斷繳貸款。Before considering a loan, build an emergency fund covering 6 months of living expenses. For example, if monthly expenses are 40K NTD, prepare at least 240K NTD cash to avoid defaulting due to emergencies (job loss, illness).

2. 月付金/收入比控制2. Payment-to-Income Ratio Control

理財規劃的黃金法則:The golden rule of financial planning:

單一貸款:月付金不超過收入的 35%Single loan: Monthly payment should not exceed 35% of income

所有負債:總月付(含信用卡)不超過收入的 50%All debt: Total monthly payments (including credit cards) should not exceed 50% of income

結論:投資更划算,保留現金投資Conclusion: Investing is better, keep cash invested

但要考慮:投資有風險,若無法承受波動,還是還貸款更安心。However: Investments carry risk. If you can't tolerate volatility, paying off the loan provides peace of mind.

七、避坑指南:常見錯誤與陷阱7. Pitfall Guide: Common Mistakes & Traps

❌ 錯誤 1:只看月付金,忽略總成本❌ Mistake 1: Only Looking at Monthly Payment, Ignoring Total Cost

某銀行推出「40 年房貸,月付更輕鬆」方案。800 萬貸款,20 年期月付 4.2 萬,40 年期僅 2.5 萬。看似划算,但:A bank offers a "40-year mortgage, easier monthly payments" plan. For an 8M NTD loan, 20-year term costs 42K/month, 40-year term only 25K/month. Looks great, but:

20 年總利息:205 萬20-year total interest: 2.05M NTD

40 年總利息:400 萬(幾乎翻倍!)40-year total interest: 4M NTD (nearly doubled!)

建議:盡量縮短年限,除非現金流極度緊張。Tip: Shorten the term as much as possible, unless cash flow is extremely tight.

❌ 錯誤 2:寬限期的甜蜜陷阱❌ Mistake 2: The Sweet Trap of Grace Period

房貸常見「前 2 年寬限期」,只繳利息不還本金,月付金減半。但寬限期結束後:Mortgages often offer a "2-year grace period" where you only pay interest, halving monthly payments. But when it ends:

剩餘年限縮短(18 年還 800 萬本金)Remaining term is shortened (18 years to repay 8M NTD principal)

月付金暴增 50-80%Monthly payment surges 50-80%

總利息增加 10-20%Total interest increases 10-20%

建議:寬限期僅適合短期現金流困難,非長期策略。Tip: Grace periods are only suitable for short-term cash flow issues, not a long-term strategy.

600 分以下:可能婉拒或利率 4%+Below 600: May be rejected or rate 4%+

建議:申貸前 3 個月避免:(1) 頻繁申請信用卡;(2) 預借現金;(3) 遲繳帳單。Tip: 3 months before applying, avoid: (1) Frequent credit card applications; (2) Cash advances; (3) Late bill payments.

結論:聰明貸款,財務自由第一步Conclusion: Smart Borrowing, First Step to Financial Freedom

貸款不可怕,可怕的是不了解貸款。掌握本文的核心概念:Loans aren't scary—not understanding them is. Master these core concepts:

理解計算原理:等額本息 vs 等額本金,選擇適合自己的方式Understand calculation principles: Fixed payment vs declining balance, choose what suits you

看懂 APR:總成本才是關鍵,別被低利率騙了Understand APR: Total cost is key, don't be fooled by low rates

善用提前還款:前期還款效益最大,但注意違約金Use early repayment wisely: Greatest benefit early on, but watch for penalties

控制負債比例:月付金/收入比不超過 35%Control debt ratio: Payment-to-income ratio should not exceed 35%

避開常見陷阱:寬限期、超長年限、忽略總成本Avoid common traps: Grace periods, extra-long terms, ignoring total cost

記住:貸款是工具,不是負擔。合理運用貸款,搭配良好理財規劃,可以加速實現人生目標(購房、創業、教育)。但過度負債會壓縮生活品質,甚至陷入財務困境。Remember: Loans are tools, not burdens. When used wisely with good financial planning, loans can accelerate life goals (home ownership, business, education). But excessive debt can squeeze quality of life and even lead to financial distress.

🧮 立即試算您的貸款方案🧮 Calculate Your Loan Plan Now

使用我們的免費貸款計算器,輸入本金、利率、年期,立即查看等額本息 vs 等額本金的詳細對比,規劃最佳還款策略!Use our free loan calculator. Enter principal, rate, and term to instantly compare fixed payment vs declining balance methods and plan the best repayment strategy!